Does Homeowners Insurance Cover Hidden Water Damage in Florida?

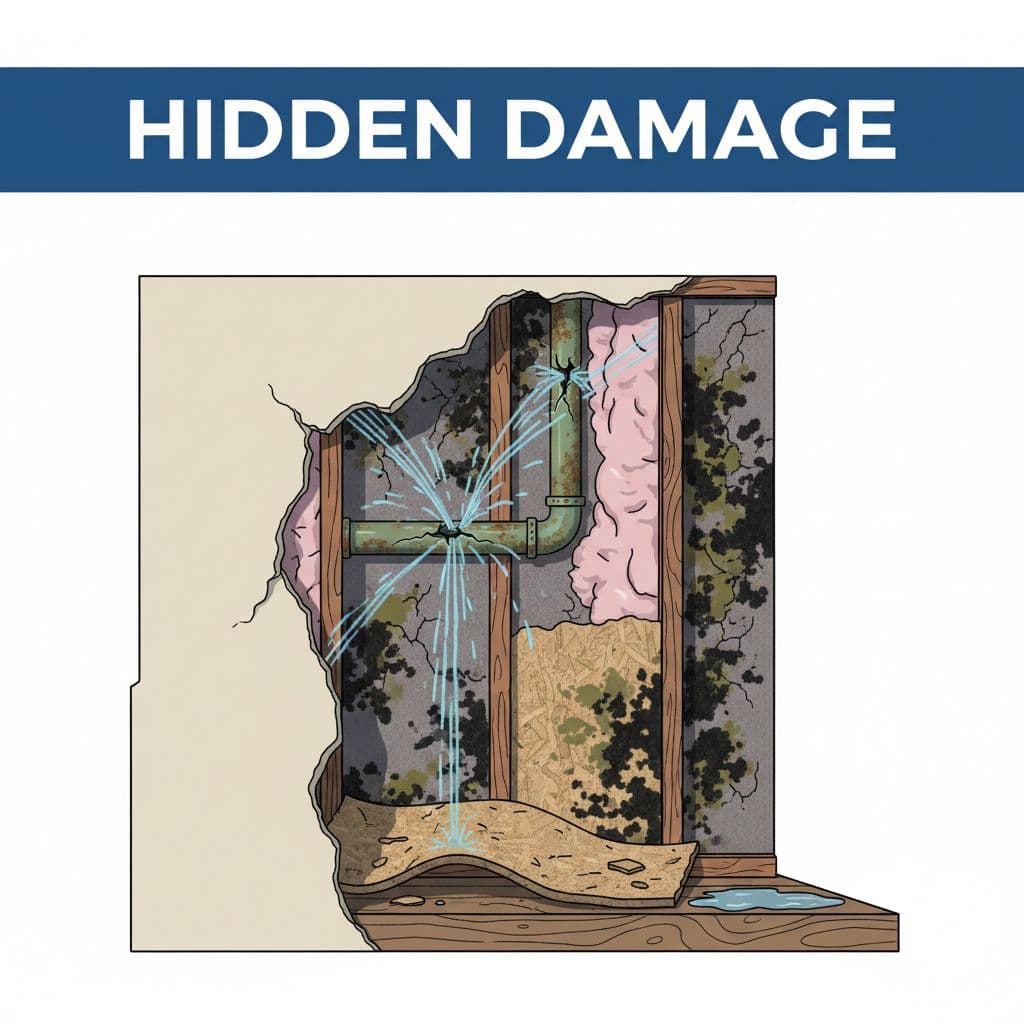

Hidden water damage can sit behind a wall long after the first drop lands. By the time you notice a stain, warped floor, or musty smell, the repair bill may already be climbing.

If you live in Florida, homeowners insurance may help, but only when the cause, timing, and policy language line up. A sudden burst pipe is treated very differently from a slow leak that kept dripping for weeks.

That gap causes a lot of confusion. Florida heat, storms, and older plumbing make the question come up often, so the safest move is to act fast, save proof, and know which parts of the policy matter before repairs begin.

When hidden water damage in Florida is usually covered

Most standard Florida home policies, especially HO-3 forms, cover sudden and accidental water losses unless the policy excludes them. The Florida homeowners insurance toolkit explains that this common form covers perils not specifically excluded, including accidental discharge or overflow of water or steam.

That matters when the water starts inside the home. A supply line can burst behind a wall, a water heater can fail in a garage, or an appliance hose can split under a cabinet. In those cases, the visible puddle may be small while the wet insulation, drywall, and flooring keep spreading the damage out of sight.

If the leak starts suddenly, the hidden damage can still be part of the claim. Insurers often pay for the source of the loss and the related repairs, although the exact scope depends on the policy. Some policies also pay for tear-out work, which means opening walls or flooring to reach the broken line.

Storm damage can fit too when wind-driven rain gets in through a damaged roof. The cause matters more than the stain on the ceiling. A clean-looking paint line can hide soaked framing, and a small leak can touch several rooms before anyone notices.

That hidden part is where many claims begin.

When Florida policies usually push back

Coverage usually gets pushed back when the leak looks old. A slow drip under a sink, a corroded supply line, or repeated moisture around the same base cabinet can point to a maintenance issue instead of a covered loss. Once the insurer sees a pattern, the claim can get narrowed or denied.

Flooding is a different problem. Standard homeowners insurance usually does not pay for storm surge, rising groundwater, or water that comes in from outside the home. The flooded street photo below is a reminder that a house can take on water from the street and still fall outside a normal policy.

Photo by Connor Scott McManus

That matters in Florida because heavy rain can pile up fast. A roof leak from wind may be one thing. Water pushed into the home by a rising canal, a storm surge, or outside runoff is another.

Sewer or drain backups often need separate coverage too. Without an endorsement, the claim may be limited even when the water damage is obvious. Mold can also become part of the fight, since a hidden leak in Florida humidity can create growth long before anyone sees it.

Why hidden leaks cause disputes

Hidden leaks cause disputes because the timeline is hard to prove. Was the pipe burst sudden, or had water been moving through the wall for weeks? Did the homeowner report it right away, or wait until the floor buckled? Those details often matter more than the visible damage.

Adjusters look for clues in the materials. Corrosion, rust, swollen trim, peeling paint, and mold growth can all suggest the leak happened over time. That does not mean a claim is dead, but it does mean the insurer may argue the loss was gradual.

Policy wording can shift the result as well. Citizens’ HO-3 comparison guide shows that some Florida forms use water-loss limits, tear-out rules, and water-backup endorsements, and some even tie water-damage coverage to the age of the dwelling. That is one reason two homes with similar damage can get different answers.

A homeowner who sees a ceiling stain may think the issue is simple. The insurer may see an old moisture pattern. In hidden water damage claims, the history of the leak can matter as much as the repair estimate.

What to do the moment you find the damage

Once you spot hidden water damage in Florida, move fast but stay calm. The goal is to stop more water, document the scene, and avoid making the claim harder to prove.

- Shut off the water source if you can do it safely. If the leak is from an appliance, unplug it too.

- Take wide shots and close-up photos before you move anything. Include the ceiling, baseboards, flooring, and the source if it is visible.

- Write down when you found the leak, who found it, and what you did next. Save texts, emails, and voicemails if they relate to the loss.

- Keep receipts for plumbers, fans, drying equipment, and temporary fixes. Those costs can matter in a covered claim.

- Call the insurer quickly and ask what they want next. Ask whether they need an inspection before major repairs start.

If drywall is soft or flooring is lifting, do only the work needed to keep the damage from spreading. Some policies limit repairs started before notice or inspection, so don’t rush into major demolition.

A fast report and clear photos often matter more than a long explanation later.

That record helps show the damage was sudden and that you tried to limit the loss, which is exactly what an adjuster wants to see.

When a professional inspection helps

Professional help can make sense when the damage is hidden, the stain keeps growing, or the room smells musty. A plumber can trace the source. A restoration contractor can measure moisture and dry the structure before the problem spreads.

That work is more than cleanup. It creates a record of what was wet, what had to be removed, and what stayed in place. If the damage is behind cabinets, under flooring, or inside a wall, that kind of inspection can show the true scope.

In Florida, speed matters because warm air and trapped moisture can feed mold quickly. If you see visible mold or smell it after the leak, a mold inspection may be smart before rebuild work starts. A small leak can turn into a bigger repair if the hidden cavities stay damp.

A licensed remediation team can also help keep the affected area contained while the claim is being reviewed. That can matter when the insurer wants proof that the work was reasonable, necessary, and tied to the water loss.

General claim scenarios that show the difference

These are general scenarios, not promises about any one policy. The same stain can lead to a very different answer depending on the cause.

| General scenario | Insurance view | Why it matters |

|---|---|---|

| Burst supply line behind a sink, found the same day | Often covered | The loss looks sudden and accidental. |

| Slow leak under flooring for months | Often denied or limited | It looks gradual and tied to maintenance. |

| Wind-driven roof leak after a storm | Sometimes covered | The cause may be a covered wind event. |

| Storm surge or rising water enters the home | Usually not covered | Flood coverage is usually separate. |

| Sewer backup without an endorsement | Usually not covered | Extra water-backup coverage may be needed. |

A burst line and a slow leak can leave the same patch of damage, but the insurer may treat them as two different losses. That is why hidden water damage claims are won or lost on timing, proof, and policy language, not on the size of the stain.

Before repairs begin, check whether the claim is built on a covered source of water, an exclusion, or an endorsement that changes the limit. Hidden damage is messy, but the policy language is usually the cleanest place to find the answer.

Policy details to read before you file

Start with the declarations page, the water-damage exclusion, the deductible, and any endorsements for backup or tear-out. Those pages tell you what the policy actually promises, not what the ad or renewal notice suggested.

Some Florida forms also put limits on water loss based on the age of the dwelling, so older homes may need a closer look. If your home has had past plumbing repairs or repeated leaks, ask how the insurer will read those facts.

Also check whether mold, cabinets, flooring, and finish work have separate limits. A leak behind a wall can touch all of them, and the policy may treat each part of the claim differently.

Before you file, it helps to know the difference between a covered source of water and an uncovered one. A small leak can sit near a big exclusion, and that boundary is what shapes the claim.

Conclusion

Hidden water damage in Florida may be covered when it starts suddenly, gets reported fast, and fits the policy wording. Slow leaks, neglect, floodwater, and uncovered backups are the reasons many claims get cut down or denied.

The safest path is simple. Stop the water, document everything, notify the insurer, and get a professional inspection when the damage is behind walls, cabinets, or flooring.

In water claims, the stain is only the clue. The policy language, the cause, and the timeline decide the outcome.

{kind=link}